COMPOUNDING |

Time is your biggest ally as an investor. That's because the more time you have to invest, the longer your investment can compound, or grow in value.

Compounding is a financial phenomenon that makes time work in your favor. It's what happens when your investment earnings are added to your principal, forming a larger base on which earnings may accumulate. And as your investment base gets larger, it has the potential to grow faster.

The younger you are when you start investing, the more you will benefit from compounding. Let's say you begin investing at age 25, putting $200 a month in a tax-deferred retirement plan earning 6%. Your friend starts investing in the same plan at 45, but puts away twice as much money as you — $400 a month. At age 65, you will both have invested a total of $96,000, but your investment would have grown to $400,290, while your friend's investment would be worth only $185,740. The reason your investment has grown so much more than your friend's — even though you both invested the same amount of money — is because of 20 extra years of compounding.

A 6% return on your investment isn't guaranteed, and, if you invest in stocks, chances are your portfolio will earn more than 9% in some years, and may even lose money in others. But, if you invest in stocks for the long term, history is heavily in your favor: From 1926 through year end 2011, large-company stocks as a group have provided an annualized return of 9.8%, based on the performance of the Standard & Poor's 500 Index.

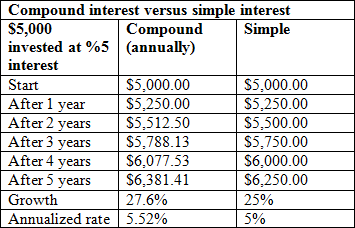

Some investments — such as money market accounts and certificates of deposit (CDs) — increase in value by earning interest. The interest income you earn may be calculated in two ways. It may earn simple interest, which means the interest is figured on your principal alone, or it may earn compound interest, which means the interest you earn on the investment also earns interest.

The way the interest is calculated will affect the yield, or what you earn on your investment. The more frequently the interest is compounded, the higher the yield, or the rate of return on your investment.

For example, if you had $5,000 in an account that paid 5% annually in simple interest for five years, you'd earn $250 a year, for a total of $1,250 in interest. In this case the interest rate and the yield are the same — 5% per year.

But the same $5,000 investment paying 5% interest compounded annually for five years would produce a total of $1,381.41 in interest. Because you're earning interest on your interest, the yield — an average of 5.52% per year — is higher than the interest rate.